Promotion of Accounting Reform as the most

effective Pathway to a Fairer Safer and more Prosperous Society. Comment

and Support from all quarters is Sought to straighten out NZ's problem

This month we focus on Institutional Shareholders. They have come in the spotlight in connection with the recent withdrawal of the proposed merger of NZ's biggest private sector electricity generator, and large retailer of the stuff, Contact Energy, with its 51% parent from across the ditch, Origin Energy.

Its not directly an accounting matter but accounting issues are never far away from such a topic.

The stories suggest that Institutional Shareholders are flexing their muscle in respect to company control and we ask whether this potentially very influential sector is really up to it. The flexing expression is attributable to Adam Bennett in the NZ Herald of 8 July. Whether the Institutions scuttled the merger is unclear but they seem to have come out firmly against it and the jobs of Contact's independent directors might be on the line.

Mr Bennett produces a list indicating a wave of institutional or small shareholder activism in the new millennium. The sole entry for 2004 is Lindsay Pyne leaving the board of Telecom(NZ), after this director came under serious criticism at Telecom's 2003 annual meeting which appointed him. The criticism, in turn, related solely to the accounting treatment in allocating income from zero-coupon bonds in the 1990 Bank of New Zealand accounts which Mr Pyne signed as Managing director and then later defended to the Securities Commission. We claim that the income allocation is entirely an accounting issue, and while Mr Pyne knew and understood what was going on with the bond income, and deserved what he eventually got 14 years later, it is the professional accountants at the heart of this scandalous allocation that deserve to incur the greatest wrath from both the Institutional investors and the NZ Herald. But despite Peter Garty, the 1990 Bank of New Zealand external auditor, hitting the headlines in recent times for commercial activity of most dubious ethics, not a murmur of criticism have we ever detected from either sector of Mr Garty's 1990 role, let alone calls for him to be removed from his senior Telecom accounting job, which should happen. The NZ Herald was been reminded of Mr Garty's 1990 doings but is ignoring them.

This NZ Herald article of 8 July gave considerable coverage the Investment Manager of the Accident Compensation Corporation, Nicholas Bagnall despite this institution being rather raw Government. Despite also Mr Bagnall being around when ACC squandered half a million bucks buying National Mail days before that company gave up on the mail business. It is rather obvious that postal services is something of a natural monopoly but when NM rolled out and bolted down a whole set of smart new blue post boxes that did not put up any warning flags at ACC we are asked to believe. As Mr Bagnall tells it they did not subscribe to NM initially but were impressed by the appointment of Mr Peter Fitzsimmons to the board of NM some time later. ACC staff might have got to know Mr Fitzsimmons through his appointment to the board of @work(NZ), a state entity set up by the then National led Government in its proposed reorganisation of the accident compensation function. But impressed as they were with Mr Fitzsimmons the ACC investment staff would know that his major position was as chairman of the retirement village developer and operator Metlifecare, the founder and largest shareholder of which was Mr Cliff Cook. Obviously these two men got on well with one another or they would not have so co-existed.

After National Mail had not reported for some time ACC made its purchase of NM shares in excess of $500,000, the vendor being Mr Cook. It is not known if they knew who the vendor was but one would think that they would have been cheeky enough to ask and if told would realise that Mr Cook would likely have access to better information than they had. In any case they knew that they were buying blind on a risky venture and the possibility of the other party, whoever it may be, having leaked information was considerable.

The ACC chairman at that time of the NM purchase, and Minister of Finance when the 1990 BNZ annual accounts were released despite his knowing that the Bank had liquidity problems, David Caygill , said that ACC had muffed it in undertaking this purchase but according to Mr Bagnall there was no mistake and the loss was an unavoidable consequence of the risk taking needed to get a good overall return.

ACC apparently have an extensive list of brokers from which they choose one to represent them in any particular trading. Presumably this list is partly so they can throw their brokerage money around fairly evenly and partly so there is always a broker available who has no conflict of interest with the other parties to the proposed trade and so able to give good independent advice. It would seem that on being advised that the NM share parcel was available by the vending brokers C S First Boston, ACC engaged the brokers Credit Suisse F B to advise them and negotiate the potential purchase, or perhaps it was the other way around. Having four words in their name is a bit clumsy so these firms condense a couple of words to initials you see.

That brings us on to the name Credit Suisse First Boston Asian Merchant Partners which has come to light as the promoters of an initial public offering of Feltex Carpets Ltd. CSFB(AMP) apparently bought the equity capital of Feltex over time from 1996 for an aggregate of $22m and then sold it via this public issue around June 2004 for over $200m and the value of this equity in the public hands has now almost returned back to the $22m. Quite an imposing roller coaster! The Securities Commission exempted CSFB from nominating a share price and telling about themselves by way of the Commission's notice No 2004/103 so the promoters could have a good old book build it would appear. It is hard for critics to lampoon the share price when they don't know what it is. The Commission does not seem to be interested in taking a closer look at the prospectus at this stage. Perhaps the chairwoman is away fulfilling her international obligations as re-elected chairwoman of the IOSCO. NZ possibly has to wait for her attention. They only get 3 years to prosecute for insider trading and in the Tranz Rail case they missed the bus by a country mile.

There is a copy of the Feltex prospectus of 2004 on its web site. We have had a look at it and are not impressed. The Auditors, as one might expect if a publication turns out to be controversial, were Ernst and Young,. There is no identification of the partner or partners involved as with public sector audits, just a signature as if the firm was a person.

The Promoters were actually Credit Suisse First Boston Private Equity, a complex offshoot of CSFB which we found out is a long standing Swiss institution, the place where the Fay Richwhite partners also tend to hang out these days we understand. We think the best place for such gnomes is probably the back garden if only they would stay there.

The prospectus is dated 5 May 2004 and Feltex's financial year ends on 30 June. The most controversial page of the prospectus is probably 86 which claims to be a Consolidated Statement of Prospective Financial Performance. It looks all very concise but the question is who decided on the prospects and how? There are some clues in the accompanying narrative. The June 2004 result is "forecast". The first three quarters of that year had transpired and been measured (the first half had been reported upon but we should have been told the results of the third quarter) and we are told the final quarter had been forcasted from the trend of the previous three. The 2005 year result is "projected". A projection we are told is not a forecast but just what it is is hard to decipher. There are plenty of warnings against interpreting the forecasts and projections in pretty much any way, which we are much inclined to agree with, and that rather brings up the question of what the forecasts and projections doing there in the first place. Investors will be inclined place significance upon them because they are there. The word "realistic" is used in describing the projection however and the promoters need to be held accountable for that.

It is the sales that are the tricky bit and profit is very sensitive to the sales it would seem. The expensive bit it would seem is not the materials that go into a carpet but the productive capacity sitting there waiting to be fully used. Earlier drops in profit have been attributed to sales downturns to a large extent. The 2005 projected sales were set at 3.8% above the 2004 forecast. It is said that only a 1% increase in total carpet demand was allowed for. The other component would seem to be the 3% inflation allowed for. One would expect inflation would apply to most all expenses deducted to get the EBIDTA yet the increase in EBIDTA for 2005 indicates little increase in these expenses. (EBIDTA = earnings before interest, depreciation, tax, and amortisation or some such)

But although a 1% increase in total market demand might be conservative by long term historic standards the requirement for any product does not necessarily move forever upward and should never be assumed to do so. Background information provided states that the biggest driver of Feltex carpet sales was new house construction in Australia. There seems to be reference to this boom-bust indicator having been applied to the sales prospective. We have come across this web page: http://www.abs.gov.au/AUSSTATS/abs@.nsf/mf/5609.0?OpenDocument of the Australian Bureau of statistics which gives this graph for the number of borrowing commitments for construction of owner occupier housing in that fine if prejudiced nation. We accept that not everyone having their house built will need to borrow but think most will.

Conveniently May 2004 the date of the prospectus is shown on the graph. One can see that there has been quite a downturn in these commitments up until then. One would expect that there would be and drag of several months between committing to a loan for construction and going to buy the carpets, so that downturn, which had been going on for six months and all but the last month should been known to the promoters, should have been impacting right when the prospectus was being finalized, we submit.

In fairness we show a second graph which is of borrowings for purchases of new owner-occupier dwellings in Australia which is less clear-cut. We think these might be smaller homes and the volumes are not quite as big. The carpets may well be in at the time of such purchase borrowings but there was a big peak at the start of 2004.

We claim that the basis of the sales projections for 2005 was not appropriate and historic long term growth was not really relevant.

But it is the 2004 sales forecast that we wish to criticize most. There were only two months of the year to go. They do not seem to say what the 3rd quarter sales (to 31 March) were. We suspect that this is usually the lowest quarter and they have forecast the second half of the year $12m below what the first half was. We will attribute that $12m drop to the third quarter so that the second half forecast of $159m is comprised of $74m and $85m. The 2005 annual accounts show total operating income for the year to June 2004 to be $329m compared to $335.5 forecast on page 87 of the prospectus. This $6.5m million discrepancy presumably relates to the final quarter already on third gone and forecast 8% too high.

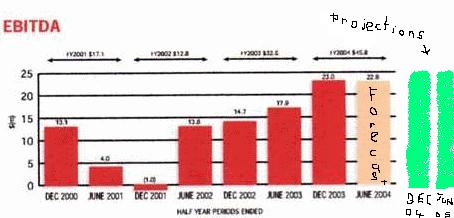

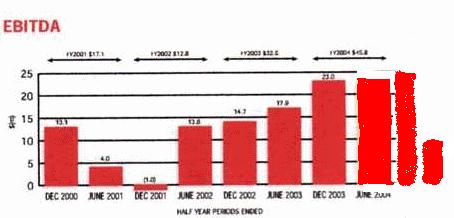

We consider also the EDITDA earning figure. We copy a graph of this measure for recent half years as shown on page 82 of the prospectus. The half year forcast to 30 June was shown in the pinkish shade and but not the prediction for the 2005 year which has been stated. We have added this as best we could as shown in green. Despite the dip that bottomed below the zero line the promoters seem to suggest that the wave effect has gone and this surplus measure has reached a stable Utopia.

We also show this graph with the actual figures as given in the 2005 annual accounts. We can now see the continuation of the wave effect which an honest promoter would have alluded to as being the likely pattern. They said the trend series had been adjusted for discontinued operations. In one sense it can be argued that because these particular operations will not affect future profits their historic effect is not relevant. But probably aspects of the business will keep cropping up as having become unprofitable and eventually needing to be closed down. If such things are going to lower future profits the effect of earlier equivalents on past profits should be shown also.

We concede that the EDITDA held up longer than what would be expected from the drop in house construction, but these auditors, in conjunction with budding gnomes did prop up the 1990 Bank of New Zealand profit and no doubt could do such a thing again.

We accept that Feltex has copped anti-NZ- business sentiment in Oz, probably triggered by the full purchase of ANSETT Airlines by Air New Zealand (we have our suspicions about what motivated those directors to do that) which was soon followed by groundings and the collapse of Ansett, and is symbolised by the failure of the The Warehouse and Telecom businesses over there. The promoters and auditors of the offer for Feltex should have noticed this. NZ should perhaps have nationalized a few Australian banks and chain stores operating here to help make the Australian consumers grow up and play fair. The tail has got to be allowed to vibrate the dog.

We leave the feltex issue.

The Feb 2002 Tranz Rail share sales are a most damning instance for the reputation of institutional investors. The shares halved in value until taken over by Toll Holdings. The sharemarket was rising over that time so the losses born were about $100m. There is not one good reason for this purchase by the institutions and we can only speculate that personal rewards to some of the actual decision makers might have been involved. Sure the Tranz Rail accounting was pathetic but outwardly so and these investors are not dumb. We have covered this topic recently.

Main line institutional investors do not appear to have been extensively involved in the 2004 Feltex issue, although amongst Feltex's twenty largest shareholders is National Nominees (NZ) Ltd and Citibank Nominees (NZ) Ltd. These two companies masked the real identity of the purchasers of the 50m Tranz Rail shares in 2002 we have referred to.

The NZ Herald needs to be careful not to launder the reputation of institutional investors when reporting on their increasing power.

The Dominion Post's apparently new business commentator, Marta Steeman in the 1 July edition seems to back criticism by institutions and others of Contact Energy's independent Phil Pryke. She says Mr Pryke twice made hasty decisions in recommending that takeover offers for the company be accepted, and calls on him to put himself up for re-election at the next AGM despite him having done so at the last one. Surely he has been well placed to come to a conclusion without waiting to hear what others might say. It is not a very independent action to wait and align oneself with the opinion of another independent appraiser as Ms Steeman suggests he should have done. And the idea of a director's term is to allow them to strike out without having to be constantly accountable to shareholders.

Contact, like Telecom, is much dependant on the Government and hence public opinion deciding how much profit it should have. There is no saying when the Government might act to curtail profits, probably through greater price competition from its SOE puppets with which Contact competes. Reports on future profitability can thus have little precision.

Ms Steeman needs to base her opinions more on facts and logic and not her impressions of personalities and reputations. In a 15 Nov 2005 article under her name it was proclaimed that New Zealand's "exports per capita were almost half that of Australia and 2.5 times less than the United States". The Dominion Post stuck to its guns when a complainant tried to point out that NZ's exports per capita were in fact significantly higher than those two countries. It thought it could get clean away with a complaint to the Press Council quoting correct figures and their source, because the article could be interpreted as quoting Bank of New Zealand chairman, Kerry McDonald , concerning the exports. Apparently the Council does not care if a newspaper quotes invalid facts given by someone else without questioning their reliability. But the complainant happened to stumble on Mr McDonald's source material which showed the statement was a mis-quote and the Dominion Post was required to print a 700 word article on the matter which had no reference to the complainant's export data or any other correct version and only conceded that the statement complained about was "inaccurate" and hence the complaint was upheld. It printed this on a back, general readership, page.

But the Council determination printed puts emphasis on the fact that neither Mr McDonald or anyone else had complained, (possibly due to numerous articles on the pressing need to export) so that readers will draw the impression that although "inaccurate" the statement on NZ's exports per capita as stated by the Dominion Post on 15 Nov was substantially correct and the complaint was trivial and not really justified. The determination remains indefinitely on the Council's web site so defaming the complainant and it seems Ms Steeman, her employer, and the Press Council care not.

Better assessment and assessors of institutional investors is required.

The scandalous Audit Cert of the

1990 BNZ annual accounts - Take a Look from Here And

then learn about the Securities Commission here

who reported on the affair. We also background the role of the Institute of Chartered

Accountants of NZ in ignoring the affair. It might go back 10 years

but many players still maintain high office, collectivly protecting

themselves at the expense of others.

------------------------

Structure and Operation of an alternative Accounting Organisation

designed to shun dishonesty.

Conveniently May 2004 the date of the prospectus is shown on the graph. One can see that there has been quite a downturn in these commitments up until then. One would expect that there would be and drag of several months between committing to a loan for construction and going to buy the carpets, so that downturn, which had been going on for six months and all but the last month should been known to the promoters, should have been impacting right when the prospectus was being finalized, we submit.

Conveniently May 2004 the date of the prospectus is shown on the graph. One can see that there has been quite a downturn in these commitments up until then. One would expect that there would be and drag of several months between committing to a loan for construction and going to buy the carpets, so that downturn, which had been going on for six months and all but the last month should been known to the promoters, should have been impacting right when the prospectus was being finalized, we submit.  We claim that the basis of the sales projections for 2005 was not appropriate and historic long term growth was not really relevant.

We claim that the basis of the sales projections for 2005 was not appropriate and historic long term growth was not really relevant.  We also show this graph with the actual figures as given in the 2005 annual accounts. We can now see the continuation of the wave effect which an honest promoter would have alluded to as being the likely pattern. They said the trend series had been adjusted for discontinued operations. In one sense it can be argued that because these particular operations will not affect future profits their historic effect is not relevant. But probably aspects of the business will keep cropping up as having become unprofitable and eventually needing to be closed down. If such things are going to lower future profits the effect of earlier equivalents on past profits should be shown also.

We also show this graph with the actual figures as given in the 2005 annual accounts. We can now see the continuation of the wave effect which an honest promoter would have alluded to as being the likely pattern. They said the trend series had been adjusted for discontinued operations. In one sense it can be argued that because these particular operations will not affect future profits their historic effect is not relevant. But probably aspects of the business will keep cropping up as having become unprofitable and eventually needing to be closed down. If such things are going to lower future profits the effect of earlier equivalents on past profits should be shown also.  We accept that Feltex has copped anti-NZ- business sentiment in Oz, probably triggered by the full purchase of ANSETT Airlines by Air New Zealand (we have our suspicions about what motivated those directors to do that) which was soon followed by groundings and the collapse of Ansett, and is symbolised by the failure of the The Warehouse and Telecom businesses over there. The promoters and auditors of the offer for Feltex should have noticed this. NZ should perhaps have nationalized a few Australian banks and chain stores operating here to help make the Australian consumers grow up and play fair. The tail has got to be allowed to vibrate the dog.

We accept that Feltex has copped anti-NZ- business sentiment in Oz, probably triggered by the full purchase of ANSETT Airlines by Air New Zealand (we have our suspicions about what motivated those directors to do that) which was soon followed by groundings and the collapse of Ansett, and is symbolised by the failure of the The Warehouse and Telecom businesses over there. The promoters and auditors of the offer for Feltex should have noticed this. NZ should perhaps have nationalized a few Australian banks and chain stores operating here to help make the Australian consumers grow up and play fair. The tail has got to be allowed to vibrate the dog.