To Contact Us

To our page bach through previos editions click here Index is in right hand column

To view our conclusive evidence that the Feltex IPO was instigated by the major political parties to rob investors to cheat Olympic medals click here

mid March 2014 Edition

Well the Feltex shareholders action against those responsible for the 2004 Feltex IPO (Houghton V Saunders) has started in Wellington. We were there on the first day. We were reasonably happy with the plaintiff’s case as it was outlined.

We called in for a while on Tuesday 25th. Dr Newberry, an expert witness for the plaintiffs was being cross-examined. The topic was alleged window dressing of sales figures by bringing sales into an accounting period which would normally occur later. The most common tactic appears to have been to invite retailers to buy there typical July (say) purchase in June but pay for it as normal (perhaps August). Well that’s OK if it has been going on consistently for ages but if it has been brought in during an accounting period the period sales will be overstated and adjustments need to be made. Dr Newberry calculated $2m sales had been bought forward in a month and $8m in the same month in the next year. That probably means a $6m false rise in sales. The defendants were tending to argue that the practice was going along all the time, and that the extra credit was generating more sales. No doubt they were partly right. But say a Feltex supporter has been renewing their carpet every 10 years and 8 years have elapsed. They are probably going to buy next year or the year after. Even although their carpet is in the condition expected for 8 years old they might see this credit offer of Feltex and decide to indulge and renew the carpets in the house. It is probably good news except the expected sale next year or the year after will quite certainly not now take place. It is a bit of a burden putting in new carpet. It is easy to suggest that “we are on the up and up” when in fact sales have been captured early and a big down is in store.

The other factor is the cost of the credit or other inducements that might be offered just before the end of an accounting period. A firm might run at a loss on these sales just to get more sales into the period. An adjustment to sales would need to be made for forecasting purposes even if the extra sales were at the expense of a competitor.

We were also there on the second day of the hearing. The referencing of documents seemed to be the matter at issue. There seemed to be two electronic systems in operation and participants were only interested in the paper record. The plaintiffs seem to be going to cover the field quite well but there seems to be going to be a matter of “pleading” when it comes closer to the verdict. One gets the feeling that only matters mentioned in an initial accusation made several years ago when the case first started will be relevant.

The hearing is far too long for us to cover the lot.

Now back to impressions of the first day.

It is a case revolving around documents with the IPO prospectus being the prime document.

A series of accounting experts are being called including Sue Newberry and Alan Robb who were once at Canterbury University but we think were pushed out of the country by Helen Clark. Ms Clark did not want any advocates of accuracy hanging around these parts. She was out to rob the ignorant to further her causes.

No mention has yet been made of the Securities Commission although all the accusations are in defiance of the Commission’s statement that there was nothing significantly wrong with the IPO. The plaintiffs need to come out and say the Commission is corrupt and a corrupt Commission was deliberately appointed by the Government and the Government deliberately set out to rob the public to raise funds for Olympic cheating.

Unless the full story is told they stand to lose.

A witness is going to say that that the 1% p.a. increase in market share adopted was unrealistic and market share had been consistently falling since the year 2000.

Nothing much has been said about the 1% increase in market size allowed for though.

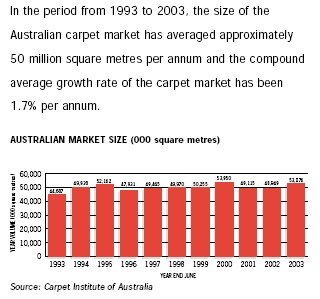

We refer again to this extract from page 37 of the prospectus which we show on the left.

It shows the Australian carpet size for the previous 11 years. But it only uses two of those sizes (those on the extremities of the graph) to calculate the “average” growth. This is easily verified by taking the 1993 size and growing it by 1.7% compounding over 10 years. You get the 2003 size. The 1993 size is the lowest at least since 1989. This is crooked analysis and the crooked Securities Commission knew it. Taking these figures for the 10 latest years and using the forecast function on Microsoft Excel the size for the 2005 year is forecasted to be 3% less that the actual size for the 2003 year, not 3.4% above it as Feltex here “calculate” it or 2% above it as Feltex adopted for its projections of year 2005 results. Feltex inferred on page 91 of the prospectus that the 1% p.a. increase in revenue due to increased market size adopted for the calculation of its projections for its 2005 year was less than what the trend of the sizes for the previous 10 known years would indicate. This was quoted by the Securities Commission at paragraph 61(a) of its report on the Feltex IPO Just observing that such a statement was made is of course not sufficient in carrying out a review of an IPO. The Commission has got to ascertain if what was said was correct which it certainly was not. This is not an error of judgment. What is the point of mentioning that this was said if not to infer that it was valid? It is obvious that no genuine investigation has taken place. It is also obvious that the Commission would not fake an investigation unless that is what they had offered to do to get the plum job from a crooked Government

The difference between a 2% rise and a 3% fall from year 2003 is about $17m a large part of which would constitute profit. Feltex had chosen not to say what recent history of change in market share was, nor did the Securities Commission say what it had been. But it can be calculated that Feltex’s share had fallen from the previous year by 5% of its sales in both the 2002 and 2003 years. At paragraph 62 the Securities Commission says it received information and explanations supporting the 1% p.a. of sales assumed accounting share increase. But it gives no clue as to the nature of such information and explanations. Do not believe it. If a 5% p.a. of sales reduction due to reduced market share had been provided for that would have reduced projected sales by $30m and projected profit by a similar amount. Feltex purchased the Melbourne factories and production capacity of Shaw Industries in the year 2000 but it seems it did not take over any of Shaw’s carpet brands. Shaws was free to compete against Feltex by way of overseas manufacture and it no doubt determined that this was economically viable before it sold the factories. Feltex had the productive capacity and the liability of looking after staff but no markets. The Securities Commission knew all this but had agreed to support the Government by giving the robbery a clean bill of health. The Securities Commission quorum which handled the Feltex IPO was Jane Diplock, Annabel Cotton, Keitha Dunstan, and Joanna Perry. Six of the ten Commission members including this quorum were women at the end of the 2004 year the report of which is here. Complaints about women being appointed to anything were “unacceptable” so Miss Clark had a free hand in setting up her crooked Commission. In addition at paragraph 15(k) of the Securities Commission’s report we learn that Kevin Simpkins was the Commission’s retained accounting expert. This crook has been given a host of high profile positions and awards to protect him from accusations and prosecution. He hangs out at Victoria University of Wellington as did Keitha Dunstan before she returned to Oz. The page of his “credentials” is here. It does not say that he comes from South Africa (he did as did Feltex’s chairman and chief financial officer at the time of the IPO) and no doubt helped the apartheid Government to produce propaganda to help keep it in power. With the change in Government there he has had to come here to continue his trade.

The court case action being taken by a large number of Feltex Carpets Ltd lead by Eric Horton is seemingly confirmed as being on and starting 17 March this year. It is important the Court hears of the Government supervision of this crime.

The case will be heard in the Wellington High court under Justice Dobson we understand. Until recently it was being managed from the Christchurch High Court under Justice French. The appellant shareholders have a Chistchurch QC Austin Forbes still representing them.

Justice Dobson gave a speech at the opening of the NZ Supreme Court in 2004. The Supreme Court has jurisdiction over all activity in NZ from 1 January 2004. The Feltex IPO was in April 2004. A corrupt judiciary has been put in place with the introduction of the Supreme Court who no doubt have pledged to ensure that those associated with the Feltex IPO (and some similar scams) do not get into trouble and that the scam and its purpose (winning Olympic gold and silver medals) is not exposed. The Securities Commission has also been stacked with corrupt people for the same purpose.

Justice Dobson presided over the case which convicted four Lombard directors, including two former Justice ministers of making false statements in a prospectus. Justice Dobson apparently found large parts of the crown evidence unproven and the Court of Appeal increased the sentences which he imposed.

Although it most corruptly “did not find” the massive Feltex IPO robbery the Securities Commission nevertheless detected and very accurately and thoroughly reported the misreporting by Feltex of the nature of its bank debt in its half-yearly report to 31 December 2005. The debt was classified as “non-current” when it was in fact current ie repayable at short notice. The Ministry of Economic Development brought charges against 5 Feltex directors because of this report of the Securities Commission. But the female judge found these directors not guilty and got made Chief District Court judge as reward for her indiscretion.

to top of page vAdvertising section

We link to: Accounting Page - Comprehensive Accounting Resources and Directory.Internet Web Directory - The internet's fastest growing directory of the best web sites. Fully searchable and updated regularly. We Advertise:

Books

Case studies of ICANZ coverups 2 Ernst and Young report to Dairy Co shareholders

Pokemon

Gifts

Cars

Toys

MP3

Videos

Dolls

Garden tools

Jewelry

------------------------

Structure and Operation of an alternative Accounting Organisation designed to shun dishonesty.

Suitable Objectives

Register of Members

Members Forum - Topical * open to all meantime: Plenty of Opinion

Magazine Plans

Need an Accountant? or Prepared to Change?

Users Forum * have your say

Ready to Join?Offering some Help?

Knowledge Tests * being developedInformation Bulletins

Why it is being Proposed

What's Wrong with the existing accounting body?

So called BNZ Auditan extensive case study Current Attitudes of Existing Institute

Visit our Advertising page from

Here